Traditional payment systems are riddled with delays, high fees, and limited accessibility. Even today, cross-border payments can take up to 5 days and incur fees as high as 7%! Web3, with its decentralized infrastructure and innovative protocols, is poised to disrupt this outdated model.

Key Takeaways

- Traditional payment systems are slow, expensive, and inaccessible to many, while Web3 offers faster, cheaper, and more accessible payments using blockchain technology.

- Challenges for Web3 payments include scalability and liquidity, particularly for micropayments.

- PayFi enables instant, borderless financing with high liquidity by using tokenized receivables as collateral.

- PayFi allows businesses to access funds owed to them (receivables) immediately, rather than waiting for payment terms, improving cash flow and efficiency.

- Huma, the first PayFi network, facilitates this by allowing financial institutions to lend against these tokenized receivables.

Web3 promised us a world where financial transactions are instantaneous, borderless, and accessible to anyone with an internet connection. For the longest time, none of the innovations could deliver on that promise — sadly, not even Bitcoin.

However PayFi, representing a new frontier in RWA tokenization, has emerged as the long-awaited solution.

In this article, we will go into the intricacies of Web3 payments and explore how PayFi is supercharging payments by letting users capture the time value of money.

The Outdated Infrastructure Of Traditional Payments

Traditional payments rely heavily on centralized institutions like banks, credit card companies, and payment processors. These entities act as intermediaries, facilitating transactions between parties.

As a result, international bank transfers (remittances) can take 3-5 days to process, with multiple intermediaries and regulatory checks slowing the process. In 2023, the global average cost of sending remittances stood at 6.2%, significantly higher than the UN Sustainable Development Goal of reducing it to 3% by 2030.

Fees accumulate through processing costs, currency conversions, and intermediary charges, making cross-border transactions expensive and time-consuming.

While this system has been reliable for decades, it is simply not keeping pace with modern demands.

Moreover, access to these traditional financial services isn't universal. A significant portion of the global population (over 1 billion as per the World Bank) remains unbanked or underbanked due to various barriers like geographical location, lack of necessary documentation, or simply the high costs associated with banking services.

Many TradFi systems rely on outdated technology, making them slow, rigid, and vulnerable to security breaches. Adding to the problem is a lack of transparency in transaction processing which leads to disputes, especially in international payments where funds can take days to clear.

The limitations of traditional payment infrastructure are increasingly apparent. Businesses and consumers alike demand faster, more secure, and cost-effective payment solutions.

The New Age Infrastructure Of Web3 Payments

Enter Web3 payments. Instead of relying on a central authority, transactions occur directly between users on a peer-to-peer network. This is made possible through distributed ledger technology, where each transaction is recorded on a blockchain that's transparent and immutable.

A significant enabler of borderless payments is stablecoins.

Stablecoins combine the benefits of blockchain technology with the stability of traditional currencies, making them ideal for everyday transactions and cross-border payments.

This infrastructure is built on smart contracts and cryptographic principles, ensuring secure and transparent transactions without the need for intermediaries. This speeds up the transaction process and significantly reduces costs. For example, sending cryptocurrency to someone across the globe can happen in minutes, if not seconds, with minimal fees compared to traditional wire transfers.

However, Web3 payments still face some challenges concerning scalability and liquidity.

For domestic micropayments, many mainstream blockchains (like Bitcoin and Ethereum) are expensive. Newer blockchains, like Solana, are solving the scalability issue effectively.

Liquidity is another key factor. A highly liquid payment system ensures that assets can be quickly and easily exchanged without causing significant price movements. This stability is essential for both everyday users and investors, fostering confidence in the system.

Platforms like Arf specialize in enhancing liquidity in cross-border payments by using stablecoins for instant settlements. Arf eliminates the need for pre-funding, which traditionally locks up capital for weeks.

Stellar is another innovator in the global remittances space. The Stellar Consensus Protocol (SCP) ensures low-latency transactions and allows financial institutions to issue and transfer assets like fiat tokens seamlessly. Notably, IBM adopted Stellar for its blockchain payment solutions.

A borderless payment solution breaks down geographic barriers that have long limited economic participation. By enabling seamless cross-border transactions, individuals and businesses can engage in global commerce more freely, promoting economic growth and inclusion.

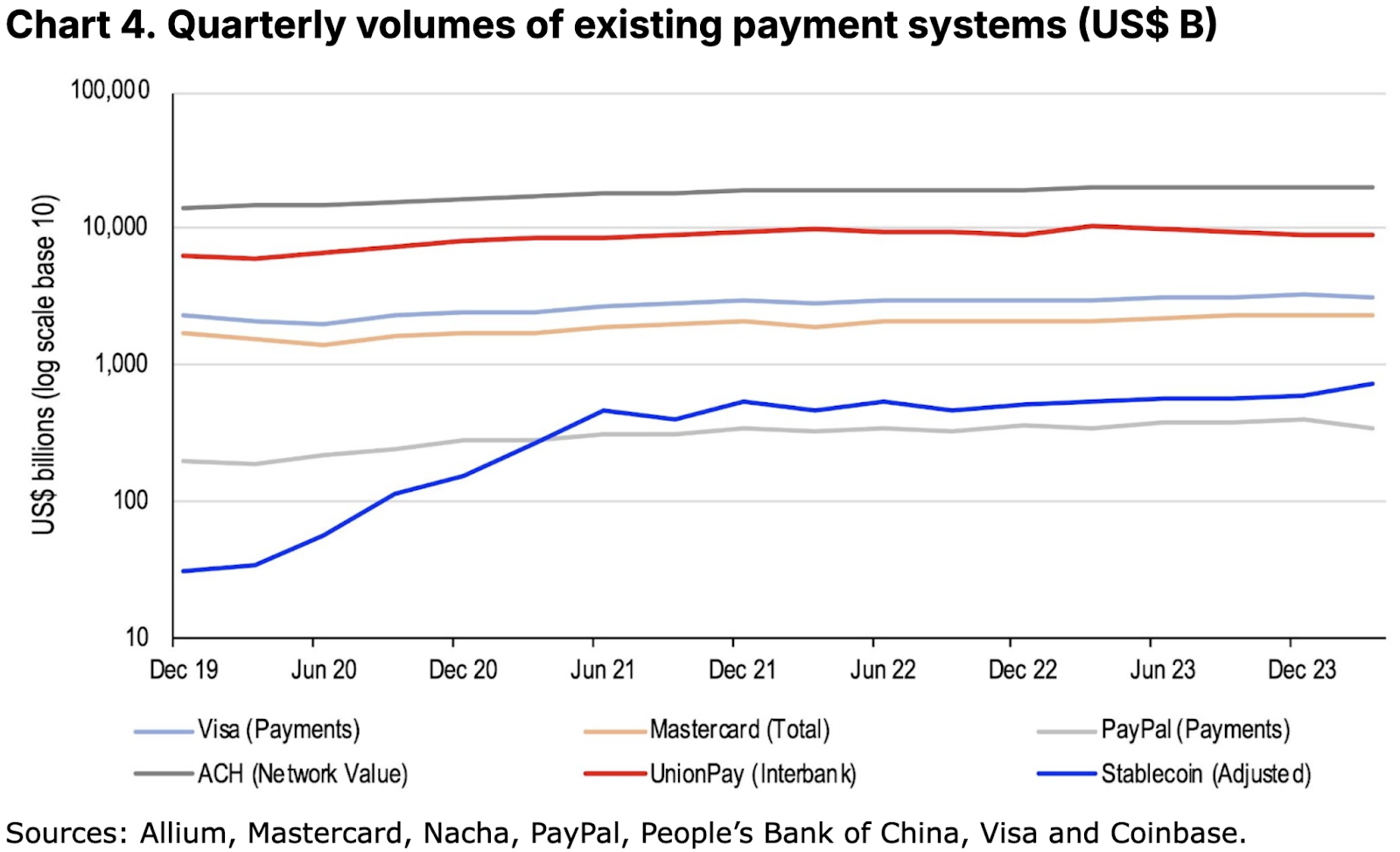

The chart shown below illustrates the rising usage of stablecoins in payment systems against conventional payment methods.

The Need For PayFi

Despite the promise of Web3 payments, there's a clear need for a solution that further enhances their capabilities. This is where PayFi comes in.

PayFi uses blockchains and stablecoins to drastically improve the efficiency of existing payment financing solutions and enables new experiences not possible in Web2.

PayFi achieves these transformations by providing immediate liquidity, removing the delays and complexities of traditional finance systems. It gives businesses and individuals control over when they pay and get paid, promoting financial freedom. It is a force to transform blockchain’s power into massive real-world impact. Huma, the world’s first PayFi network aims to make this a reality using blockchain’s borderless traits and Huma Pools to provide:

- Near-instantaneous transactions: No more lengthy processing times.

- Enhanced liquidity: Businesses can access funds quickly and efficiently.

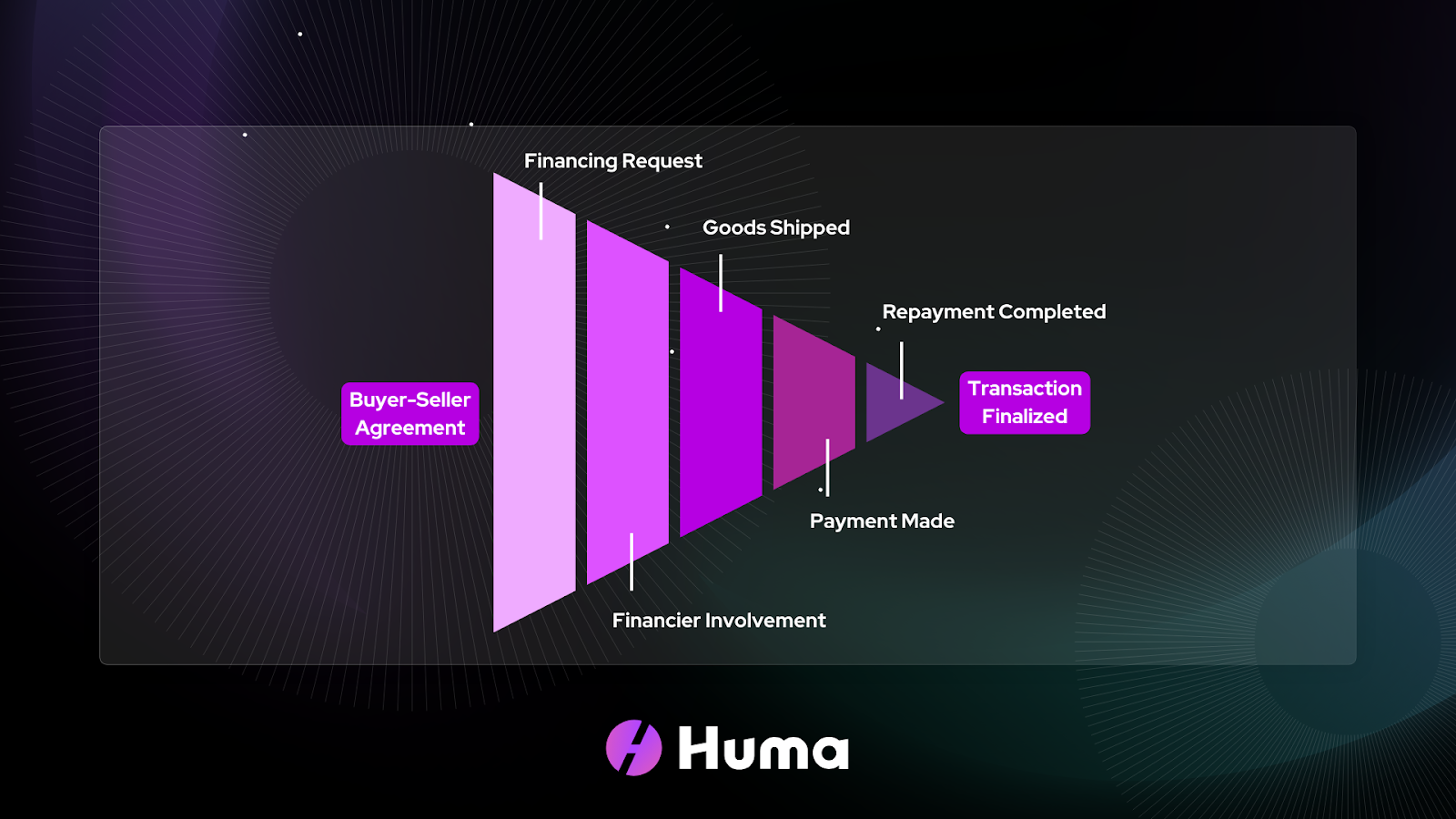

Here’s how cross-border payment financing typically works:

- The deal: A buyer in one country orders goods from a seller internationally.

- Financing request: The buyer or seller (or both) might need financing to cover costs like production, shipping, or to bridge the gap while waiting for payment.

- Enter the financier: A bank, financial institution, or specialized fintech steps in to provide a loan, credit line, or other financing solution. This could involve letters of credit, factoring (selling invoices), or other trade finance tools.

- Goods shipped & payment made: The seller ships the goods, and the buyer, using the financing, makes the payment.

- Repayment: The buyer repays the financing according to the agreed terms, and the seller receives the funds.

Seems straightforward. The problem is that conventional financiers do not accept a wide variety of collateral. And the seller has to wait for days to receive the payment while the goods have already been shipped. So, the seller cannot use the money they are owed immediately, causing them to lose value (and opportunities) because of the waiting period.

Huma addresses this by providing receivable-backed credit lines. Let’s illustrate this with an example scenario.

Consider a business that has delivered goods to its customers. The customers have agreed to pay $100,000 in 30 days. This outstanding amount is known as a ‘receivable’ as it is owed but not yet received.

However, the business has already incurred an expense by delivering the goods. So, their net profit is in the negative at least until the invoice is cleared. This lack of liquidity may hinder the business from pursuing new growth opportunities. In such a case, the business can use the receivables as collateral to finance its growth and operations, which involves opening a receivable-backed credit line.

Here's how it works:

- Application: A business applies for financing through Huma, presenting the receivables as collateral.

- Assessment: A financial institution reviews the business's request and the underlying receivables.

- Funding from pool: Upon approval, the financial institution borrows the necessary funds from a Huma Pool, using the tokenized receivables as collateral.

- Advance rate: Just like with a regular business, an advance rate is applied. So, the financial institution might borrow 80% of the value of the receivables from the Huma Pool.

- Disbursement: The financial institution then provides the financing to the business.

Conclusion

The future of payments is unfolding before our eyes. PayFi, with its innovative approach to using tokenized receivables for efficient credit lines, is setting a new precedent and unlocking practical use cases for RWAs. Businesses that are heavily reliant on cash flows and the time value of money can greatly benefit from it.

As the first PayFi network and leading the charge in cross-border payment financing, Huma is enabling businesses to “seize the moment” and unlock value by bypassing intermediaries.